PicPay offers loan options inside the app that can feel fast because the full flow is digital, from simulation to repayment.

Approval is not guaranteed because every offer depends on credit analysis and your profile at the time of request.

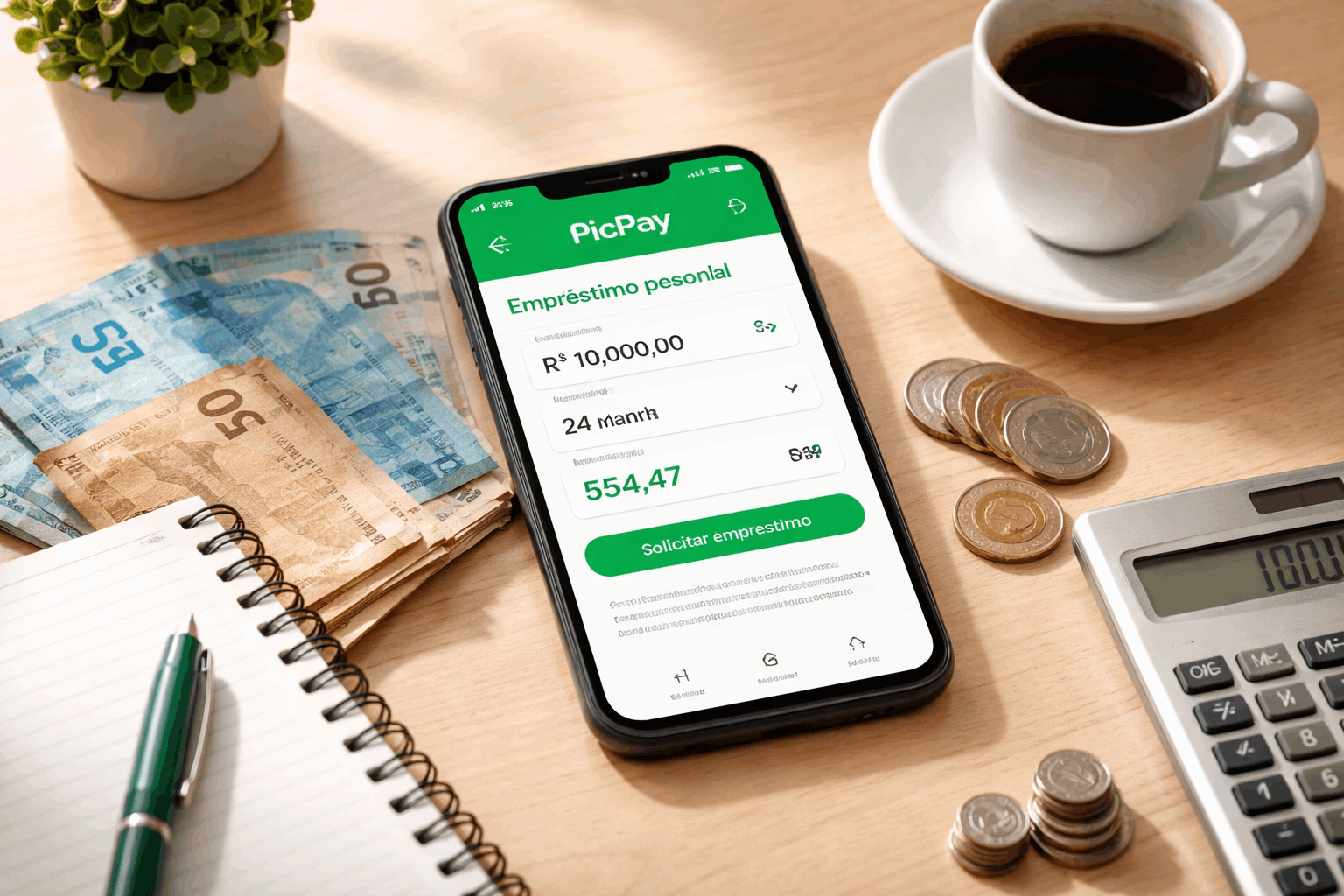

The app shows the rate, term, and total cost before you confirm, so you can decide with the full numbers in view.

How PicPay loans work in practice

PicPay’s loan experience usually starts with a pre-offer or simulation inside the app based on eligibility.

Once you choose va alue and term, you review the contract terms and confirm digitally.

After approval, the money is deposited into your PicPay account, and installments are paid in the app.

The availability of each loan type can vary, so the app is the best place to confirm what is live for your account today.

Personal loan inside the app

A personal loan is usually presented with a simulation screen that displays the monthly rate and installment value before you accept.

PicPay explains that the monthly interest rate is defined by analysis of your profile and cannot be changed after contracting.

PicPay has also communicated that offers may start from 1.99% per month, but the final rate depends on the person and can change over time.

Other loan modalities you may see

Depending on your profile, PicPay may show additional credit products or partner flows that still follow the same logic of simulation → analysis → contract.

The key difference between modalities is usually the repayment method and the risk level, which influences the rate shown in your simulation.

If a modality is available, your app will display the full cost details and the effective total cost (CET) before confirmation.

Eligibility and what tends to be required

Eligibility is driven by internal and external checks, so two people can see different limits and rates.

Your offer can change if your income, debts, or payment history change, even within the same year.

Most digital lenders also use fraud-prevention checks, which is why data consistency matters during onboarding.

The safest approach is to keep your registration data updated and run a simulation only when you are ready to compare terms.

Basic eligibility signals

You typically need an active PicPay account in good standing to view loan options in the product area.

Credit analysis generally considers payment behavior, existing debts, and identity validation during the flow.

If you do not see a loan offer, it often means there is no available proposal for your profile at that moment.

Data and documents commonly requested

Digital credit flows often request confirmation of identity data, and sometimes income-related information depending on the offer.

If the app requests documents, submit clear images and avoid mismatched information to reduce delays in analysis.

Keep an eye on in-app status updates so you do not miss a pending verification step that pauses the process.

Interest rates, CET, and total cost

There is no single fixed “PicPay loan rate,” because the rate is typically personalized and shown in-app.

Before contracting, you should check the interest rate, IOF, installment amount, term, and CET displayed in the simulation.

PicPay explains that the interest rate shown is tied to profile analysis and is not changeable after you agree.

If you want a quick comparison, focus on CET because it consolidates the main charges of the credit operation.

Where to find the exact rate for your offer

PicPay states the monthly interest rate is presented according to analysis of your profile and is part of the contracted terms.

Your simulation should show the rate and the total amount to be paid, and you should only continue if you accept those numbers.

PicPay has published that some offers may start from 1.99% per month, but the final rate depends on your profile and can vary.

IOF and mandatory charges in Brazil

PicPay’s help center reminds that loans in Brazil include IOF (Imposto sobre Operações Financeiras).

It lists IOF as 0.38% over the total amount plus 0.0082% per day, based on the number of installments you choose.

Because IOF affects total cost, you should always read the CET and contract summary before confirming.

CET and why it matters for “quick approval” loans

CET is a consolidated rate that helps you compare credit offers beyond just the monthly interest rate.

A loan can look “cheap” by rate, but still be expensive when you include taxes, fees, and term length, which CET helps reveal.

Use CET to compare alternatives, then decide if the speed and convenience are worth the final total you will pay.

Step-by-step application and approval flow

The fastest path is usually a clean simulation followed by immediate confirmation, without missing verification steps.

You should expect the process to include identity checks, selection of value and term, and digital acceptance of the terms.

If your information is consistent, the app flow can feel simple because there is no branch visit or paperwork delivery.

If the system requests extra validation, approval can take longer because your case may move to additional review.

Simulate your loan before you commit

Start by checking the loan area and opening the simulation so you can see the available value and term options.

Review the interest rate, IOF, CET, and installment schedule shown, because those are the decision-making numbers.

Stop if the total cost is not acceptable, because a “quick approval” is only good if the repayment fits your budget.

Credit analysis and digital contracting

After you confirm the simulation, the request goes through credit analysis, which can approve, decline, or request more info.

If approved, you accept the contract terms shown in-app, and the interest rate becomes locked to that contract.

Keep screenshots or confirmations of the terms so you can track the exact conditions you accepted if you need support later.

Disbursement and repayment

Once contracted and approved, the money is typically credited to your PicPay account, and repayment happens by monthly installments in-app.

Set reminders and keep balance planning tight because missed payments can increase costs and affect future credit.

If you need to renegotiate, use official PicPay support channels and avoid third parties asking for “unlock” payments.

Support, official contacts, and safety checks

PicPay lists SAC (general support): 0800 025 8000, with 24-hour availability according to its help center.

For escalations after prior support attempts, PicPay lists Ouvidoria: 0800 025 2000, on business days from 9h to 18h.

Located at Av. Manuel Bandeira, 291, Condomínio Atlas Office Park, Vila Leopoldina, São Paulo/SP, CEP 05317-020.

Final thoughts on fast approval and smart borrowing

PicPay can be convenient when you want a digital loan flow with clear in-app simulation and contracting.

Speed should never replace checking the rate, IOF, CET, and installment schedule shown before acceptance.

If the numbers fit your budget, follow the app steps carefully and keep your account data consistent to reduce delays.

Disclaimer: This article is for informational purposes and does not constitute financial advice or a guarantee of approval. Loan availability, limits, and rates can change, and the final conditions are the ones shown in your PicPay simulation and contract.